Fresh Life Advice aims to aid you in taking control of your money by increasing your savings and reducing your spending. FLA will encourage you and help you along your journey to financial independence. I am not a licensed financial advisor. More importantly, FLA does not condone in investing your money in something you do not understand. My goal is give readers a better understanding of his or her own personal finances.

Welcome to the 6th FLA Guest Blog Post! Today, we explore how to retire early. Thank you to Rachel from Annuity.org for sharing this helpful article.

Rachel Christian is a professional journalist who has covered business, local government and education since 2014. She is a Certified Educator in Personal Finance with FinCert, a division of the Institute for Financial Literacy.

Rachel is also a member of the Association for Financial Counseling & Planning Education and a past member of the American Finance Association. She holds a bachelor’s degree in journalism from the University of Southern Indiana. Her leadership role at her college newspaper led to a professional career writing public service-style pieces about taxation proposals and government audits to inform everyday citizens.

Rachel strives to communicate important, complex topics including finance and investments to help readers understand and apply valuable knowledge to their lives. Rachel also contributed to Evansville Business, which covered major financial developments and economic opportunities in Indiana’s third largest city.

Early Retirement

Retiring early is a dream for many, and it is possible to make it a reality. With careful planning, dedication, and a bit of luck, you can retire early and enjoy the rest of your life. Here are some tips to help you retire early and live the life you have always wanted.

The first step to retiring early is to create a budget and stick to it. This will help you determine how much money you need to save each month in order to reach your retirement goals. It is important to consider all of your expenses, including taxes, insurance, and other costs. Once you have a budget in place, you can begin to save money each month.

The second step to retiring early is to invest wisely. Investing your money in stocks, bonds, and mutual funds can help you grow your retirement savings. You should also consider investing in real estate, which can provide steady income and tax benefits. With careful planning and research, you can make wise investments that will help you reach your retirement goals.

Finally, you should make sure to take advantage of any retirement savings plans offered by your employer. Many employers offer 401(k) plans, which allow you to save money for retirement on a tax-deferred basis. You should also look into other retirement savings plans, such as IRAs and Roth IRAs.

Retiring early is a great way to enjoy the rest of your life. With careful planning and dedication, you can make it a reality. With a budget in place, wise investments, and the right retirement savings plans, you can retire early and live the life you have always wanted.

How to Retire Early

Retiring early is an exciting prospect for many people, and it is certainly possible to do so with the right planning and dedication. To retire early, start by creating a budget and tracking your spending. Make sure to put away money into a retirement account each month, and consider investing in stocks and bonds to increase your savings. Additionally, try to reduce your debt as much as possible, as this will make it easier to save for retirement. Finally, consider working a side job or freelancing to increase your income and save more money. With the right strategy, you can retire early and enjoy the freedom and flexibility that comes with it.

Investing and Saving for Early Retirement

It is a wonderful idea to invest and save for early retirement. Doing so can help ensure financial security and provide peace of mind. Investing and saving for retirement early can help to maximize the potential of your money, allowing you to have a comfortable retirement.

It is important to research different investment options and to be mindful of the risks associated with investing. Additionally, it is important to save regularly and to consider the potential tax implications of your retirement savings. Overall, investing and saving for early retirement is a wise decision that can help to secure your financial future.

Depending on your priorities, your portfolio will contain various asset types that strike the appropriate balance to help you achieve your goals. The 60/40 investing strategy, for instance, may be used in your portfolio. This strategy invests 60 percent of the investor’s assets in stocks and 40 percent in lower-risk bonds.

However, you may want to think about reallocating your assets if economic conditions have a negative impact on the rate of return of this mix, as they seem likely to over the next ten years. Purchasing an annuity to act as a low-risk asset buffer may be successful and has the added benefits of tax deferral, lifetime income, and a death benefit for your heirs.

I am in favor of Social Security and Early Retirement. It is a great way to ensure that people can enjoy their later years in life without having to worry about financial insecurity. Social Security provides a much needed safety net for those who have worked hard throughout their lives and need a little extra help in retirement. Early retirement can also be beneficial for those who are able to take advantage of it, as it allows them to enjoy their retirement years earlier than they would have otherwise.

Obstacles to Early Retirement

It is admirable that you are considering early retirement. It is a great goal to set and can be a rewarding experience. However, there are some obstacles to consider before taking the plunge. These can include having enough money saved to live comfortably, having a plan for health insurance, and having a plan for how to spend your time.

Additionally, it is important to consider the impact that early retirement may have on your Social Security benefits. All of these factors should be carefully weighed before making the decision to retire early.

Health Care Costs

Is important to analyze the increasing attention being given to health care costs. In recent years, the cost of health care has been on the rise, making it difficult for many people to access the care they need. This is why it is so important to focus on reducing health care costs.

By implementing cost-saving measures, such as reducing administrative costs, increasing the use of generic medications, and improving access to preventive care, we can make health care more affordable and accessible for everyone.

Health Care Options for Early Retirees

It is a great decision for early retirees to explore their health care options. There are a variety of plans available to suit different needs and budgets. These plans can provide coverage for essential medical services and help to protect individuals from unexpected medical costs.

It is important to research the different options available and compare them to find the best plan for an individual’s specific needs. It’s highly recommended for early retirees to take the time to explore their health care options and make an informed decision that best suits their needs.

Some options are:

Employer-sponsored retiree health plans

Public exchanges established by the Affordable Care Act (ACA or ‘Obamacare’)

Private insurance exchanges

A spouse’s health plan

IRAs, 401(k)s and Early Retirement

401(k)s and Early Retirement, are all excellent options for individuals to consider when planning for their financial future. IRAs, or Individual Retirement Accounts, are a great way for individuals to save for retirement in a tax-advantaged manner. 401(k)s are employer-sponsored retirement plans that allow individuals to save pre-tax dollars for retirement.

Early Retirement is a great option for those who are able to retire before the traditional retirement age. All of these options can help individuals to plan for a secure financial future.

Why Guest Post With Us?

Guest posting allows you to gain access to our readers and serves as a way to promote your content. We do not charge for guest posting like many other blogs. We believe in the power of unique, valuable content and will not charge to promote it!

Disclosure: Fresh Life Advice is an opinion-based website. I am not a financial advisor, and the opinions on this site should not be considered financial advice.

Personal Capital: The Ultimate Tool to track your Net Worth, Budget and more.

What are your thoughts on retiring early? Let me know in the comments below.

Welcome to the 5th FLA Guest Blog Post! Today, we explore how to grow your side hustle into a full-time business. Thank you to Kathryn from Cash for Kat for sharing this helpful article.

Kathryn Rucker is a business consultant and personal finance blogger who is passionate about helping individuals and businesses scale by improving their online presence. Kat started traveling the world in 2019 and currently runs her blog and business out of Phnom Penh, Cambodia.

Cash for Kat will show you how to make cash, save cash, and invest cash. Join her on her journey to financial independence. Every month, she shares her latest articles on a range of money topics, such as: starting a business, budget travel, my investments, creating side-hustles, and more!

Your side hustle is more than just an extra income stream. It’s a business that can help you reach financial freedom so that you can live a happy life!

The problem is, if you’re not ready to take the plunge, your side hustle might not grow as big and as fast as you would hope. Unfortunately, that’s what happened to me when I first started my side hustles.

Eventually, I was able to grow my side hustle into a full-time business… And I want to help you do the same. From psychological tips to practical methods you can implement, this article has it all.

Without further ado, here is everything I learned about how to grow your side hustle into a full-time business!

An Overview of How to Grow Your Side Hustle into a Full-time Business

Of course, there are many things that can help you grow your business. If you ask 100 people what worked best for them, I’m sure you’d get 100 different answers!

That being said, you will also find some similarities in those responses. There are some aspects of business that just make sense, and you will hear them coming up time and time again.

Here are 5 key areas you can focus on to grow your side hustle:

1. Find Your Motivation

It is not a secret that running a business is hard. The only thing harder than running a business is starting one in the first place! To help keep you going during the hard times, you will need to examine your motives.

Common sources of external motivation:

Family

Money

Work Flexibility

While these are excellent sources of inspiration, they are still what we would consider external motivators. You might be wondering, what other kinds of motivation are there?

The answer is this: intrinsic motivation. And it is even more powerful than external motivation! Intrinsic motivation is doing an activity for inherent satisfaction.

So not only should you identify what aspects of the business motivate you the most, but you should also try to minimize the activities you dislike.

The feeling of accomplishment when you exceed your own expectations

The satisfaction of helping accomplish something

For intrinsic motivation, you will notice that what brings you joy is the feeling you get from doing the action itself. The focus is more on your own satisfaction and growth, rather than receiving external recognition (an award/money/etc.).

2. Implement the 80-20 Rule

The 80-20 rule is based on a simple premise: 80% of your results come from only 20% of your actions.

To put it a different way… we waste a lot of time on other tasks when it is really only a few of our actions that truly move the needle.

So how can you use the 80-20 rule to maximize your productivity? Identify the 20% that is driving the needle for you! Then do more of that and less of anything else.

For side hustles, you will often find that the 20% is related to gaining more business. In fact, this is true for most start-ups in general. The reason is that before you can have a perfect product or service… you need feedback! And the best way to get relevant feedback is from people who have used your product or service.

While it seems counterintuitive, I would actually focus more on doing outreach and perfecting your “concept” of what you are selling. This is actually one of the key differences between entrepreneurship and freelancing. When you focus on selling, you will eventually have more business than you can fulfill yourself and will need to build a team.

3. Sign Up for Freelancing Platforms

Though it is possible to make money online without experience, you will still need a way to pay your bills. To help you make ends meet, you will likely need to spend some time doing one-off projects.

Beginner-friendlyfreelancing platforms are fantastic for helping you go from a side hustle to a full-time business. Some people you meet on freelancing platforms might become long-term clients for you! At the very least, it will help you build a portfolio and gain plenty of references.

You will also gain experience managing the expectations of your clients. This can be important because there are many moving parts in a business. Using a freelancing platform helps you focus less on obtaining new clients and more on fulfilling projects in an organized way.

4. Standardize Your Offerings

As you work on various projects, you will notice that there are certain vital things that people want time and time again. This is great because you can create a standardized offering that takes much guesswork about what kind of project you will be working on.

You will also gain valuable business skills that are related to more specific aspects of your niche. This will help show your clients that you are an expert in this field, and they will trust your recommendations more.

An example of how standardizing your offerings helps you grow your side hustle into a full-time business:

When I first started side hustling, I would do freelance blog post writing. Over time I got better at this, and now I choose to sell blog content packages to my clients.

This is great because people usually pay me to write ten or more instead of writing one blog post. Another plus is that most people who want blog posts written will also need them promoted on social media. So I started to bundle this into my offerings too!

By paying attention to what people kept asking for, I created organized packages that would appeal to more than one client. This also made it easier for me to create a system to fulfill their orders faster.

5. Reflect and Improve

Every business goes through an ugly duckling phase. It is essential to focus on progress and not perfection when you are first starting your business. You do not want to face analysis paralysis that stops you from taking action.

With this in mind, create everything with the knowledge you will have to improve it at some point. Even things I thought I had done very well at the beginning of my business ultimately needed to be redone by year two.

This is because your brand identity might change, your products might change, or you get a better idea of your ideal client’s wants. In general, the business will most likely evolve from what you initially thought it was. You will also have more budget to hire professionals to help you with your logo, website, or social content.

Chances are you will not change everything in your business overnight. That is why it is important to reflect regularly and improve your various business processes.

How to Reflect and Improve to Grow Your Side Hustle into a Full-Time Business

I like to set a Focus for the month that change based on business needs. Of course, you will still have other tasks to focus on and accomplish aside from your focus task. That being said, setting the intention to knock out one big project can help prevent it from lingering in the background all year.

For example, for one month, I might focus on trying to knock out most of the social media content for the year and automating it. In another month, I plan on updating as much of the website as possible.

Keep laser-focused on the main projects that will actually help you move the needle when it comes to growth!

Final Thoughts

If you have side hustles and side projects running in the background, it can be quite easy to lose focus on what you’re actually trying to achieve. It becomes hard to tell where you want to go.

So, when you’re trying to decide whether to quit your job or stay and scale your business, I want to help you to see the bigger picture by following the tips above.

Why Guest Post With Us?

Guest posting allows you to gain access to our readers and serves as a way to promote your content. We do not charge for guest posting like many other blogs. We believe in the power of unique, valuable content and will not charge to promote it!

Disclosure: Fresh Life Advice is an opinion-based website. I am not a financial advisor, and the opinions on this site should not be considered financial advice.

Personal Capital: The Ultimate Tool to track your Net Worth, Budget and more.

What are your thoughts on solar panels and solar energy? Let me know in the comments below.

The world is slowly but surely transitioning to solar energy. Will you embrace and adapt with the change?

Welcome to the 4th FLA Guest Blog Post! Today, we explore how solar panels can help the environment and your wallet. Thank you to Chelsea from Business POP for sharing this helpful article.

Chelsea is an experienced Marketing and Advertising professional with a demonstrated history of working in the media industry. Chelsea is especially skilled in Digital Media advertising, Events, Search Engine Optimization (SEO), Search Engine Marketing (SEM), Microsoft Suite, Data Analytics, Adobe products, and Marketing Strategy.

The digital age has unquestionably arrived. Incorporating new technologies into business procedures will be critical for owners who want to grow their businesses.

Business POP will show you how to grow your business through innovation. It is aimed at small and medium-sized business owners and will offer advice on what digital enhancements to consider and how such changes can help them grow.

There has been a lot of talk about how we can help the planet and reduce the risks of climate change, and it can be a daunting topic to think about. Luckily, there are many ways that every person can do their part to reduce energy dependence and create a cleaner environment. Installing solar panels is one of those solutions. By using this alternative form of energy, you can help the planet while saving money. The process is easy and straightforward. Here, the Fresh Life Advice blog highlights the many benefits of solar, discusses if it’s the right option for you, and offers some simple tips on getting started.

Help the Environment

When it comes to doing our part to help the environment, going solar in your home or workplace can make a big impact. According to the U.S. Energy Information Administration, solar panels produce clean energy that does not produce harmful air pollution or greenhouse gasses. This is especially important for large factories that use hundreds of panels instead of standard electricity, but on an individual residence, it can also make a positive impact.

Solar panels also reduce the wasteful resources necessary to create the electricity that powers our homes. Solar panels are a type of renewable energy source that can help reduce the use of fossil fuels and water. Massive amounts of fossil fuels and thousands of gallons of water are required to generate regular electricity. Meanwhile, solar panels rely on sunlight to generate electricity, and they can be used to power homes, businesses, and even automobiles.

In addition to being renewable, solar energy is also very efficient. Solar panels can produce up to 50 times more electricity than traditional fossil fuel-powered generators. And because they don’t rely on water to operate, solar panels can help reduce the strain on our water resources. In many parts of the world, solar panels are already playing a vital role in reducing the use of fossil fuels and water. As more people turn to solar energy, we can expect these benefits to increase.

As mentioned, the way to really make an impact on our environment is to band together to help, and with solar panels, you are essentially creating an advertisement out of your home. Neighbors will be inclined to ask about the benefits of having panels installed and they may decide to buy them as well, so you are doing your part to spread the message and the environment will be better because of it.

Cost Savings

While some people may be satisfied by just knowing that they are making a positive impact on the world, the cost savings associated with solar panels is the cherry on the cake. Electric bills can be one of the most costly utilities, especially during the hottest and coldest months. According to Move.org, the average electricity bill is over $110. Luckily, solar panels can reduce that cost.

According to 2021 estimates, solar panels can save the average homeowner about $1,500 per year in energy costs, depending on your location, the amount of sun on your roof, and how much electricity you use daily. Keep in mind that you may still get a monthly bill from the electric company to keep you on the grid in case of an emergency, but it will likely be minimal.

The cost for a solar panel can vary, and the average home needs about 16 panels, so you can expect to pay anywhere from $105 to $1,500 per panel. Bear in mind the cost of the panel is based on the number of watts per panel.

Image Source: Vivint Solar on Unsplash

If you are interested in installing panels, you can get a great start by looking into the Energy Efficient Mortgage Loan program, which helps families lower their utility bills when they implement energy efficiency into their homes, which includes solar panels. This is a great program for brand-new homes or existing properties as the cost of these improvements is incorporated into your mortgage and it translates to great savings.

You can also use Renewable Energy Credits (RECs) to make your home 100% renewably powered, solar included. RECs are certificates that represent the environmental benefits of renewable energy generation. By selling RECs, solar panel owners can receive payments for the environmental benefits their solar panels provide. In addition, some utility companies offer rebates or other incentives for solar panel owners who sell RECs. As a result, taking advantage of RECs can be a great way to reduce the cost of solar panels and encourage more people to switch to renewable energy. And, of course, it’s a great way to contribute to the earth’s well-being as it reduces your greenhouse gas emissions and carbon footprint.

The Process

Keep in mind that your home may need to meet certain requirements in order to qualify for solar. For instance, your roof will need to be in good condition as the panels are heavy and need solid support. You’ll also need enough space as the average size of the collection of panels on a roof measures about 400 to 600 square feet. Finally, the best roofs are covered with standard shingles. Slate roofs tend to break, so consider that as well.

If all conditions are met, then the initial installation process is a snap and should only take a few hours. After the panels are installed, a representative from the power company will come out to inspect the system and provide a unique meter. You should see solar power generated for your home within a month from there.

Maintenance

Most solar panels come with a 20- to 25-year warranty, but that doesn’t mean they’ll last that long without proper maintenance. In order to keep your panels running at peak efficiency, it’s important to have them inspected regularly by a qualified technician. While you can do some basic cleaning and troubleshooting yourself, it’s best to leave the more technical aspects of panel maintenance to the professionals.

So, how do you go about getting your solar panels inspected by the power company? The first step is to contact your local utility company and ask if they offer this service. If not, there are a number of private companies that specialize in solar panel maintenance. Once you’ve found a company you’re comfortable with, schedule an appointment for them to come out and take a look at your panels. Be sure to give them a thorough cleaning before they arrive so they can get an accurate reading of your system’s performance. With a little bit of care and attention, your solar panels will continue to provide clean, renewable energy for years to come.

With most kinks worked out and the benefits and cost of installation now clear, this is the best time to invest in solar panels. Consider the tips and perks above and you’ll be on your way to clean energy.

Why Guest Post With Us?

Guest posting allows you to gain access to our readers and serves as a way to promote your content. We do not charge for guest posting like many other blogs. We believe in the power of unique, valuable content and will not charge to promote it!

Disclosure: Fresh Life Advice is an opinion-based website. I am not a financial advisor, and the opinions on this site should not be considered financial advice.

Personal Capital: The Ultimate Tool to track your Net Worth, Budget and more.

What are your thoughts on solar panels and solar energy? Let me know in the comments below.

When managing your health, people often forget about their financial wellness as well. It’s important to have balance, as with everything in life.

Welcome to the 3rd FLA Guest Blog Post! Today, we explore how to not only manage your health but also your financial wellness. Thank you to Amos from Do Money Well for sharing this helpful comprehensive guide.

From teaching your children how to manage their money to saving for your golden years, Do Money Well covers it all.

We all need money. However, when you don’t have enough to maintain your preferred standard of living, you can get stressed out quickly. This is especially true for middle-class Americans facing the uncertainty of soaring housing prices, skyrocketing childcare, and salaries that have not kept up with inflation. Fresh Life Advice explains that you can take hope knowing that there are things you can do to improve your financial standing, reduce stress, and relax.

To make the most of your money, here are a few approaches to try.

Money and Mental Health

According to UK-based Mind.org, there is a very real connection between your finances and your mental health. Not having enough money can leave you lying awake in bed each night, worrying about how to pay for everything – from your children’s braces to your electric bill.

Further, feeling as though you can’t keep up with others in your social circle can leave you with feelings of shame and guilt when you do splurge on the occasional night out. It doesn’t have to be that way. We often hear this idiom referred to as “Keeping Up With The Joneses.” A few changed habits coupled with self-care and a different perspective can help you reduce stress.

Many financial experts are of the opinion that before you send off your money to do the heavy lifting, you need to have an emergency savings account that will cover at least six months of living expenses.

One of the best places to store your cash is an FDIC-insured, high-yielding savings or checking account as it can generate maximum value.

A typical savings account provides an interest of about 0.01%. To put this into perspective, putting money in a checking account is equivalent to stashing money under the mattress. However, high-yield savings and checking provide interest rates that are more than 1%, which is about 1% more than what you usually get.

Save Money Without Sacrificing Your Health

It’s easy to think that saving money means giving up on everything you love and need to be well. This simply isn’t true. There are many ways that you can continue to put your health first. These include:

Meal plan. Meal planning is one of the easiest ways to keep your diet and nutrition goals. It’s also an excellent way to save money since you only have to shop once each week, and you won’t have the temptation to run to the drive-through since your food is already ready. There are many apps, such as Paprika and Mealime, that can make meal-planning easy. The Spruce Eats has a great list of different apps that can make mealtime healthier, efficient, and budget-friendly.

Exercise outdoors. Strong Home Gym estimates that the average gym membership costs more than $50. That’s $600 per year that you don’t have to spend, and tossing your fitness center card in the trash means one less bill to pay each month. Instead, plan to spend more time outdoors, which can help you with everything from weight loss to stress while giving you plenty of open spaces to walk, swim, and hike. Look for parks in your area that allow people to freely exercise. If you have a dog you want to include in your workouts, find a pet-friendly park and bring them along.

Look for free workouts online. If you can’t get outdoors to exercise, no problem. Thanks to the internet, finding workout routines and tutorials is as easy as logging into your YouTube account. Many personal trainers and exercise aficionados offer a wide range of exercise videos that can help you refine your current workout routine to learn something completely new. You can also download exercise videos to your tablet and take things outside.

Prioritize self-care. Self-care is something as simple as a warm bath or a good book at the end of a stressful day. Or, you may simply want to crash on the couch with your favorite video game or the television program you’re currently watching. Do what makes you feel your very best; you are doing yourself a disservice if you feel like anything less, and your goal is to feel better, not worse.

Shop for affordable products. Look for highly-rated kitchen gadgets, workout equipment, and other health-focused products to help you live healthier. You can check out Safe Smart Family for unbiased reviews and information on the latest products to help get you started.

Inflation is when the costs of products or services rise but paychecks don’t keep up. An increasing inflation rate can paralyze a nation’s currency value and buying potential.

In fact, inflation can reduce the wealth that you create. For instance, the present inflation rate in the United States is 2.26%. So, if you invest in a fixed deposit (FD) that offers a 3-4% return, that is not going to work.

This investment will erode your wealth. It will work against you. This is the reason investors invest in market-linked assets, such as mutual funds and stocks. These assets can outpace inflation. Top-quality stocks generate average returns between 9% and 12%. With mutual funds, you can get a return of 6% to 15%.

Buying assets is an effective way to make money and beat inflation. There are apps that provide access to top-quality mutual funds andstocks.

Earn Without Giving Up All of Your Spare Time

When you simply need to make more money, your first inclination may be to take on more hours at work or to get a part-time job. These can absolutely help, but then you continue to be defined by someone else’s time clock. Instead, consider starting your own business on the side such as purchasing a condo and renting it. This gives you flexibility and, depending on what you do, may segue into a passive income down the road.

Keep in mind here that there are a few steps you should take to get your side-gig off to a good start. One is to invest the time into researching how to file an LLC.

This will make it much easier to keep your business finances and personal finances from commingling, which can protect you from financial losses. However, each state has different LLC guidelines and regulations, so it’s important to do some research to ensure you’re following all of the required steps. If you’re feeling overwhelmed, work with an attorney to make sure all of your paperwork is correctly filed with the proper offices. Formation services can also help you with this part of the business formation and are often less expensive than a lawyer.

You also want to consider scouting ahead to hire an assistant, which can handle some essential tasks on your behalf while you work your “day job.” Entrepreneurs’ Organization suggests interviewing wisely and making sure that your assistant is someone you can trust. While you will have to put some time into growing your business, you only have to work when you want, which means you can take time off for self-care. Additionally, you could also hire a virtual assistant to help with things online, such as answering phone calls, responding to emails, and helping you with aspects of your business. Virtual assistants are particularly helpful if you don’t have a physical office and are running things from your home.

Your overall wellness and health is more than the sum of what you eat and the number of hours you exercise each week. To be truly at your best, you have to take care of yourself in all areas. This includes tweaking your finances so that you have one less worry on your plate.

Why Guest Post With Us?

Guest posting allows you to gain access to our readers and serves as a way to promote your content. We do not charge for guest posting like many other blogs. We believe in the power of unique, valuable content and will not charge to promote it!

Disclosure: Fresh Life Advice is an opinion-based website. I am not a financial advisor, and the opinions on this site should not be considered financial advice.

Personal Capital: The Ultimate Tool to track your Net Worth, Budget and more.

How do you focus on your health and financial wellness? Let me know in the comments below.

When you ask for financial advice, people will often say “make your money work for you.” But how do you do it? Well, the answer isn’t simple, and there is no one-size-fits-all solution.

Welcome to the 2nd FLA Guest Blog Post! Today, we explore how to make money work for you. Thank you to Michael from Finance-Able for sharing this helpful comprehensive guide.

Finance|able was created to fill the void in the market for approachable, intuitive finance career training.

Once you make money, it is tempting to let it sit in a savings account as you try to earn more. But by investing your money, you can make it work for you and grow over time. Investing is central to a comprehensive money management strategy.

To make the most of your money, here are a few approaches to try.

1. Open a High-Yielding Savings Account

Many financial experts are of the opinion that before you send off your money to do the heavy lifting, you need to have an emergency savings account that will cover at least six months of living expenses.

One of the best places to store your cash is an FDIC-insured, high-yielding savings or checking account as it can generate maximum value.

A typical savings account provides an interest of about 0.01%, while putting money in a checking account is equivalent to placing money under the mattress. However, high-yield savings and checking provide interest rates that are more than 1%, which is about 1% more than what you usually get.

2. Purchase Assets that Aren’t Affected by Inflation

Inflation is when the cost of products or services rises but paychecks don’t keep up. An increasing inflation rate can paralyze a nation’s currency value and buying potential.

In fact, inflation can reduce the wealth that you create. For instance, the present inflation rate in the United States is 2.26%. So, if you invest in a fixed deposit (FD) that offers a 3-4% return, that is not going to work.

This investment will erode your wealth. It will work against you. This is the reason investors invest in market-linked assets, such as mutual funds and stocks. These assets can outpace inflation. Top-quality stocks generate average returns between 9% and 12%. With mutual funds, you can get a return of 6% to 15%.

Buying assets is an effective way to make money and beat inflation. There are apps that provide access to top-quality mutual funds and stocks.

3. Create a Stream of Passive Income

Passive income means the money earned with little or no effort. When you have set it up, passive income will earn you money while you sleep. This can lead to financial independence, but having passive income streams is not a get-rich-quick method.

To create a stream of passive income, you must invest upfront — whether that investment is money or time. But it will lead to large payoffs later on.

A few forms of passive income include silent business partnerships and real estate investment. However, you can also generate money through other methods, such as making YouTube videos, or starting a blog and earning via affiliate marketing.

4. Create a Retirement Fund

Many people don’t enjoy the luxury of a pension. So, you should store your money in a retirement account. Individual retirement accounts (IRAs) and 401ks are investment accounts. This means your retirement savings are an investment in the market and can grow exponentially.

The primary idea is to leverage the money you have to make more money. As you save as much as you can, your money will work for you tax-efficiently to grow more money.

In addition to IRAs, another great option is health savings accounts (HSAs). These are savings accounts with high-deductible health insurance coverage.

When you sock money away in an HSA, you won’t lose it. If you need the money for healthcare, you can withdraw your money without paying any taxes. As you turn 65, the money in the account will transform into an IRA.

So, you don’t get penalized for using the fund for other purposes. Using the fund, you can pay long-term care premiums and Medicare costs.

5. Use Target-Date Funds

Lifecycle funds, or target-date funds, are structured to grow in assets and rebalance continuously over time to optimize your savings.

It’s safer to invest in target-date funds as it helps in managing investment risk. With target-date funds, it is also possible to structure your retirement fund when you don’t want to delve deep into setting up your portfolio.

A target-date fund is based on the fund you set up for return and your age. The funds are more diversified when you are younger. This increases your risk and increases the fund’s value. So, as you age, target-funds will readjust to become more conservative.

With a target-date fund, you can set the approximate age or year you plan to retire. Presently, many target-funds have been set up for a return in 2050. It is offered through many money lenders and banks.

The process comes with some drawbacks, but one of its primary benefits is simplicity. If you want, you can make your initial investment and forget all about it until you retire. This can be preferable to bonds, stocks, and other retirement portfolios, as it is a painless method to invest in your retirement. However, you should know which stocks to buy and when it’s the right time to invest in the stock market.

6. Choose Credit Cards with Rewards

When you use a credit card, it might feel like you aren’t putting your money to work. However, choosing a card that comes with a reward can be good for your lifestyle. For instance, airline miles can be good for people who are interested in traveling.

If you have steady cash flow and pay your bills on time, you can find great credit cards. However, if you are in credit card debt, this strategy might not be useful for you.

7. Invest in Gold and Bonds

When it comes to a conventional investment strategy, many tend to look toward gold. Like real estate, it is an asset that might appreciate steadily with time. You can buy gold and hold it in your hand. This can be an appealing option for people who prefer tangible assets.

As you consider investing, be sure to take your overall portfolio into account instead of just one investment. However, in such cases, gold can serve as a stunning piece of your financial plan. But don’t invest all your money in gold. It should only be a part of your investment strategy.

Another option is to invest in bonds, where you provide a loan to an organization that consents to pay back the debt on a certain schedule. Bonds are sold by businesses and government agencies. Usually, bonds pay off twice a year. Hence, you have a predictable income source if you invest in a bond until it matures.

Bonds are predictable and this makes them attractive in an investment portfolio. If you decide to spend on volatile investments that come with some degree of risk, bonds are a good way to offset such risk.

Your gains from the bond will not increase to the level of the riskier ventures. But they are a good foundation for your investment strategy. However, before you invest in bonds, make sure you thoroughly understand the difference between stocks and bonds.

8. Become a Silent Partner in a New Business

It can be a risky move to start your own business. However, if things progress well, it is likely to pay off.

A good way to reap the benefits of a startup without the stress of getting the business off the ground is to be a silent partner who invests capital but doesn’t take care of day-to-day operations. This method allows you to earn a cut of the profits without investing long hours.

However, if you use this strategy remember that you won’t be involved in the daily decision-making process. So you may not have as much control over your investment as you would like. And if the business tanks, you will have to bear the financial loss.

9. Eliminate Debt

The idea of making money work for you is that every dollar, penny, and dime you invest or save multiplies exponentially. However, if you have debt, the exact opposite is going to happen.

Basically, each dollar you owe will cost you more in the long run. Like many, you may think that spending large sums of money now will benefit you over time, even if it means going deeper in debt. But this can cause you to stay in debt longer, and the longer you are in debt, the more money it is going to cost you to get out.

Sadly, banks and credit card companies don’t exist to help you. The money you lose every month funds their organizations. Rather than working for you, your money is working for them.

Today, people are in different kinds of debt. With time, many have accepted debt as part of their life. But this is a mindset you should get rid of. You should not accept debt as part of your life.

Here are some ways to streamline your path to a debt-free life.

Find out exactly how much you owe. It is crucial that you own your debt. Only when you know the amount you owe and to whom, along with the interest rates, will you be able to pay them off effectively.

Develop a strategy. This takes into account the amount you owe to every company along with their interest rate. The higher the interest rate, the faster you should pay it off. Use loan tracking software to learn how much you have to pay monthly to clear your debt, including student loans. Make sure you are honest with yourself. It is difficult to eliminate your debt, but it isn’t impossible.

10. Invest in Real Estate

Real estate is not a guaranteed investment. But if you have the cash and risk tolerance, consider investing in commercial or residential properties.

There are two types of real estate investment.

Buying a single home.

Investing in land to sell or in homes or stores to rent.

Your decision to branch out will depend on the market and your desire to own rental properties. In most cases, if you can take on the added responsibility of upkeep and management, investing in real estate is a great option.

Many homeowners take real estate to be the biggest asset in their investment portfolio. However, make sure that you don’t weigh your portfolio too heavily toward a single asset.

11. Invest in Cryptocurrencies

Cryptocurrencies can also be part of your investment portfolio. However, it is a speculative holding. The value of cryptocurrency is increasing exponentially, but investing in crypto comes with high risk. If the market crashes, you lose your investment.

Cryptocurrencies like Bitcoin trade with swings of at least 2% routinely throughout the day. But people think that as cryptocurrencies are adopted by more and more people, they will continue to increase in value. Take that into consideration before you decide to invest in it.

What Is the Best Way to Make Your Money Work for You?

The power of investing money is incredible. However, you are not going to get anywhere until you get started. With every passing day, you are missing out on opportunities to grow your money.

No matter the type of investment you make, seeing results will take time. Hence, we recommend getting started as soon as you can to make your money work for you.

We have provided a list of investment strategies, but you should only go for the ones that work for you. Identify your risk profile and long-term goals. Decide on a plan where you will not have to take more risk than you’re comfortable with.

Remember, investing is about carefully following strategies to a robust financial future.

Why Guest Post With Us?

Guest posting allows you to gain access to our readers and serves as a way to promote your content. We do not charge for guest posting like many other blogs. We believe in the power of unique, valuable content and will not charge to promote it!

Disclosure: Fresh Life Advice is an opinion-based website. I am not a financial advisor, and the opinions on this site should not be considered financial advice.

Personal Capital: The Ultimate Tool to track your Net Worth, Budget and more.

How do you make your money work for you? Let me know in the comments below.

Happy one year blog anniversary to Fresh Life Advice! One year ago, I opened the doors of FreshLifeAdvice.com to the world.

Of course, these doors are electronic and metaphorical.

As a teenager, I can remember using some super cool website called Myspace.com to learn about HTML coding and website building. Myspace was the first social network to reach a global audience, but we all know how the rest of that story ended…

Rest in peace to Myspace as we pour one out for Tom.

Soon, Mark Zuckerberg took over the social media sphere. With roughly 2.89 billion monthly active users as of the second quarter of 2021, Facebook is now the biggest social network worldwide. In the third quarter of 2012, the number of active Facebook users surpassed one billion, making it the first social network ever to do so.

The internet, social media, and technology, in general, are rapidly changing. I had always wanted to a piece of that pie. FLA was my chance of making a small contribution to the big world wide web.

How FreshLifeAdvice.com Was Born

After college, I wanted to fill my free time with a project that would be beneficial to the general public.

I was already writing anything and everything to escape from the daily struggle of the corporate world. Lengthy emails to friends and colleagues, forum posts about stocks, and even personal journal entries.

FLA was born with the mission in mind to help 10 million people with their own path to financial freedom. It sounds crazy, but every life-changing invention also sounded crazy before it revolutionized its respective industry.

As of January 2021, there were 4.66 billion active internet users worldwide – 59.5 percent of the global population. Of this total, 92.6 percent (4.32 billion) accessed the internet via mobile devices. Six in every ten people around the globe now use the internet…

Sure, the internet had plenty of personal finance blogs, but they all had a similar theme. Older retired bloggers who already had a large nest egg just didn’t seem relatable to the younger crowd about to embark on an arduous start to their careers. To be fair, they did inspire me to envision a prosperous future.

The millennial generation is who I wanted to reach, because, well…I’m a part of that crowd.

The mid-20s person sits at a fork in the road. It’s the age when the world presents a choice: head down a path of continuous stress and financial woes, or set yourself up for a lifetime of money mastery.

My net worth steadily grew after the Post-2008 financial crisis. Having this credibility might help people take my advice seriously, so I purchased the domain FreshLifeAdvice.com through Bluehost for any aspiring website owners.

The goal was to put a fresh perspective on personal finance. Hence, Fresh Life Advice was born.

The Great Blogging Experiment – One Year Later

I then spent the next six months nervously designing the site. Hey, I had some good-looking shoes to fill!

Of course, the design wasn’t actually the 6-month hang-up. Truthfully, I was terrified of going live.

What if nobody likes my writing? What if nobody cares what I say? And what if the only visitors are me and my mom, again?

Publishing all your thoughts and opinions for the world to see is scary enough. Baring all on a subject as taboo as money is even scarier.

Against my better judgment, on September 01, 2020, the blog you’re reading right now went live. This was the post.

When I published that first article, I made myself a promise: I was going to make it to FLA’s 1st blog anniversary, no matter what, before I could give up.

I knew I enjoyed writing, but the internet is a big place. And I was just one voice in the chatter. Maybe after one year, I’d be able to tell if anyone cared.

Well, here we are. One year later. I’m happy to report that the site has been a raging success, and I have zerointentions to shut it down.

This blogging experiment has truly been one of the most rewarding projects I’ve ever involved myself in. Every time I receive a personal reader email, an inspiring article comment, or an enthusiastic Facebook share, I can’t help but get excited and marvel at the wonders of the internet.

So, I want to say THANK YOU! At the risk of sounding extremely cliché, you – the reader – are what makes this site what it is.

I’m just a guy typing some nonsense on a keyboard. You’re the one who keeps this site alive.

One Year of FreshLifeAdvice.com Blog Anniversary Statistics

299 Page views in the blog’s first month.

150 About how many of those page views came from me.

100 Page views the first day I thought an article went viral. I remember my heart pounding as I watched the page stats, refreshing them repeatedly.

697 The most page views in a single month.

8 Total email subscribers after the first 4 months.

52 Email subscribers today. (You are on the cool kids’ email list, right?)

25 Total articles published in the past year.

2,217 Average Words Per Post

470,000 Total number of words in the Webster’s Third New International Dictionary, Unabridged, together with its 1993 Addenda Section.

52,070 Total number of words written by FLA. That’s 11% of the entire English Dictionary!

82 International countries reached out the of possible total 195 countries. That’s 42% of the world!

‘Mr. Worldwide’ refers to the self-ascribed nickname of American rapper and music producer Pitbull. Soon, FLA will self-ascribe a similar nickname of ‘Mr. Personal Finance Worldwide’.

These top 5 blogger commenters certainly deserve a shout-out. They’ve supported this site from the beginning. I enjoy reading and commenting on as many personal finance blogs as I can.

The Most Popular Day is Friday, accounting for 21% of views. And the Most Popular Time is 3:00 PM, accounting for 9% of views.

There must be something about Fresh Life Advice that really gets people excited about their weekends.

The stats don’t lie. Every single human falls into one or more of the DISC personality traits so it was no surprise this appeal to many different audiences. It was FLA’s way of putting a fresh twist on personality tests and spending habits.

Conveniently, this post checks both boxes of fun and helpful.

Either there aren’t very many readers, or this post was a total flop.

Don’t answer! That was a rhetorical question.

Seriously, this was the first post on the site as well as one of the shortest articles to date. No surprise here.

I have no regrets writing it because it got the ball rolling for the rest of the blog. It also serves as a constant reminder of my purpose for blogging.

The meme stock mania was very topical, and this post was published during the midst of the hedge funds losing billions of dollars due to a short squeeze.

I really enjoyed writing these ones, and I was happy with the way they turned out. But the stats say most of these weren’t read as much as the others, so here’s to giving them a second chance!

5 Foolproof Steps for Early Retirement – These are some of the most critical practices I implement in my own life to achieve F.I.R.E. as quickly as I can.

It’s been an awesome ride so far. Here’s to many more years together!

Thank you to every single person who has read FLA and supported this site! Happy Blog Anniversary Fresh Life Advice!

Disclosure: Fresh Life Advice is an opinion-based website. I am not a financial advisor, and the opinions on this site should not be considered financial advice.

Personal Capital: The Ultimate Tool to track your Net Worth, Budget and more.

Any advice for Year 2? What are your favorite things about a blog? Let me know in the comments below.

Index funds have been touted across the finance world as the proven way to invest hard earned cash. However, the wealthy have turned their backs on passively managed index funds for other types of assets. But why? Why don’t the rich invest in index funds?

Despite popularity, the ultra-wealthy high net worth individuals aren’t as apt to invest in these low-cost funds.

What are Index Funds? What’s the Advantage?

An index fund is a mutual fund or exchange-traded fund designed to follow certain preset rules so that the fund can track a specified basket of underlying investments.

Over the long term, index funds have generally outperformed other types of mutual funds. Other benefits of index funds include low fees, tax advantages (they generate less taxable income), and low risk (since they’re highly diversified).

At FLA, we preach choosing passively managed index funds or ETF’s (i.e., NYSEARCA: VTI or MUTF: VTSAX) with the lowest expense ratios (less than 0.15%) in lieu of picking individual stocks, mutual funds with high fees, or actively managed hedge funds.

Let us dig into the pros and cons of index funds:

Pros of Index Funds

1. Low-Risk

Losing the principal investment is an investor’s worst nightmare. Index funds offer a low-risk option for investing in batch of stocks. They are inherently diversified, representing many different sectors within an index, which protects against deep losses. When one index is performing better than others, the index fund effectively captures these gains that individual stock picking gurus may miss out on.

2. Steady Growth

A central advantage to index funds is that they are designed for steady, long-term growth. The ideal timeline for an investor is to have their money compound forever. No one can predict the future. As a result, having so many stocks in one fund allows for diversification in addition to a self-cleansing system. The dogs are ousted, and the winners continue to ride high.

Index funds are not designed to beat the market, but simply capture the average return. Stock-picking is much harder than one would expect. For instance, U.S. News & World Report noted in 2011 that index funds tied to the Standard & Poor’s 500 (S&P 500) index generated better returns over the previous three years than almost two-thirds of large-cap actively managed mutual funds.

3. Low Fees

Index funds offer lower fees for investors than non-index funds. This means that even when a non-index fund outperforms index funds, it must perform better by a certain margin to generate returns that overcome the management fees that it charges.

Cons of Index Funds

1. Lack of Flexibility

Because index fund managers must follow policies and strategies that require them to attempt to perform in lockstep with an index, they enjoy less flexibility than managed funds. Investment decisions on index funds must be made within the constraints of matching index returns. For instance, if the returns in an index are declining strongly, index fund managers have few options to attempt to limit those losses. In contrast, managers of an actively managed fund have more flexibility to act to find better-performing options in good times or in bad.

2. No Big Gains

An index fund does not carry the potential to outpace the market the way that managed funds can. This means that if you invest in an index fund you are surrendering the possibility of a massive gain. The top-performing non-index funds can perform far better than the top-performing index funds in a given year. However, the top-performing non-index funds may vary from year to year, so those under-performing years can cancel out the over-performing ones, while index funds’ performance remains steadier.

Why invest in VTSAX or VTI?

Beats 82% of active managed funds

Expense ratio of 0.04% / 0.03%

Self-cleansing (companies come and go)

Tracks the U.S. stock market.

Buy the whole stack, instead of looking for the needles.

Why Are Index Funds So Popular?

A stock index consists of a basket of stocks that is meant to represent something else. Sometimes, this something else is an entire stock market. Other times, this something else is a section of a stock market that serves as a stand-in for either an industry or some other kind of segment.

Whatever the case, it is very common to see interested individuals put their money in an index fund, which is either a mutual fund or an exchange-traded fund that tracks an underlying index.

Index fund investing has become popular since Jack Bogle of Vanguard introduced the Vanguard 500 fund in 1976. The fund tracked the returns of the S&P 500 and marked the first index fund marketed to retail investors.

Index investing is popular for a variety of reasons:

Index investing is a very passive way of investing, which can be contrasted with more active investment strategies that see individuals buying and selling stocks on a regular basis.

It’s extremely tough to beat the market in the long run. Once taxes and trading costs are incorporated into calculations, the index funds prevail.

There is empirical evidence that shows actively managed funds consistently underperform in the long run.

Index investing is a very useful way for investors to protect themselves from non-systematic risks through means of diversification. This is due to the fact they have spread out their money rather than concentrate it in the stocks of a small number of companies.

Individual stock picking can be time consuming. Many hours of research are required before an investor has truly educated opinion on whether to invest. Index funds a practical solution that reduces the necessary time and effort.

Unless you have the knowledge, time, and patience to vet each individual company you’re considering before buying its stock, you could wind up with a portfolio that’s weighed down with bad deals and underperformers. That’s one reason why many investors tend to appreciate the beauty of index funds.

Fees Add Up

When you invest in any mutual fund, you pay a set of annual fees that add up to its expense ratio. In exchange for the actively managed fund’s cost, you are getting the expertise of a seasoned fund manager. The manager and their team will assemble a well-researched collection of stocks, put it into a neat package, and shift the fund’s holdings when they see that as a smart idea.

That doesn’t come cheap.

With index funds, by contrast, most of that work (and pricey expertise) is not necessary, so their expense ratios can be as little as one-tenth of what you’d pay for an actively managed fund. But despite the many benefits of index funds, they aren’t particularly popular among wealthy investors.

Why the Rich Tend to Look Elsewhere

Index funds are an extremely cost-effective, convenient investment choice. But they generally aim to match the performance of their associated indexes, not surpass it. The ultra-wealthy, however, may not be satisfied with that.

Instead, they turn to other money-making assets, such as private equity, art, and even IPO’s. These investments are often far riskier than your average index fund, but they have far greater upside potential. The wealthy can take on this risk because they can still get back on their feet, even after losing a relatively large sum of money. The middle and lower classes do not have this luxury.

Let’s walk through a scenario.

Imagine that you have $500,000 invested in stocks in your tax-advantaged retirement accounts. That’s probably a lot of cash for you. If your portfolio declined in value by half, or worse, it could have a major impact on your future quality of life.

But, for example, someone with an investment portfolio worth $50 million could suffer a major loss and would still be left very relatively wealthy. That allows them the freedom to take on more risk than the average retail investor would be comfortable with.

The rich can pursue high-risk, high-reward investment opportunities without worries because their wealth can make for a very effective cushion from such problems.

In fact, wealthy investors often favor actively managed mutual funds. Their iffy odds of delivering that sought-after outperformance can be overwhelming appealing despite the higher fees. The large majority of actively managed funds won’t beat the market, and over multi-year periods, the share of them that do, drops even further. By contrast, index funds often outperform active funds across different asset classes.

Other Assets

The wealthy also can more easily invest in real estate, antiques, and other less-liquid assets — whereas you probably can’t afford to take on the risk associated with buying a $100,000 piece of art you hope will appreciate in value. And in the “actively managed” sphere, the wealthy also have the ability to put money into hedge funds, which most of us are legally barred from.

In order to protect normal people, the SEC has created all sorts of rules and regulations for how companies that invest money on behalf of other people should operate. While this makes the investments safer and less volatile, it prevents the firm making investments from chasing riskier but possibly more profitable investments.

Hedge funds are not allowed to have more than 100 investors, and they are not allowed to take on any investors with less than $1 million in wealth.

The goal of hedge funds is to earn absolute returns. What this means is that they make money every year, regardless of what the stock market does. A few funds have done this, but 2008 demonstrated that most funds were bluffing in saying they were able to do that, and many of them went out of business.

Why Don’t the Wealthy Invest in Low-Fee Index Funds?

They sometimes do. But it is also easier to buy individual stocks when one is investing large sums.

Also, many wealthy people have business experience which gives them insight into economic trends and specific companies. This leads them to buy individual stocks. Whether they perform better than the indexes is not assured.

A majority of the wealthy seek for Alpha. The finance world defines Alpha (α) as excess or abnormal return over a benchmark index.

In addition, they want to diversify their portfolio across asset class and earn underlying performance return, which is different from an index fund. This has resulted in huge investment growth in the following:

Portfolio Management Service (PMS)

Private Equity

Structured Products

Hedge Funds

Art

Real Estate

The wealthy use these investment vehicles because there is a barrier to entry with high entrance costs. These risky investments generally require large buy-in costs and carry high fees, while promising the opportunity for outsized rewards.

High Risk, High Reward

Over the past 90 years, the S&P 500 averaged around a 9.5% annualized return. You’d think the rich would be satisfied with that type of return on their investments. For example, $10,000 invested in the S&P 500 in 1955 would be worth more than $3 million at the end of 2016. Investing in the whole market with index funds offers consistent returns while minimizing the risks associated with individual stocks.

But the wealthy can afford to take some risks in the service of multiplying their millions (or billions). For another example, look at world-famous investor and speculator George Soros. He once made $1.5 billion in one month by betting that the British pound and several other European currencies were overvalued against the German Deutsche mark.

Hedge funds aim for those sorts of extraordinary gains, although history is filled with examples of years when many hedge funds failed to outperform the stock market indices. But they can also pay off in a big way for their rich clients. That’s why the wealthy are willing to risk hefty buy-in fees of $100,000 to $25 million for the opportunity to reap great returns.

The one percent’s investing habits also tend to reflect their interests. As most wealthy people earned their millions (or billions) from business, they see this path as a way to continue maximizing their finances while sticking to what they know best — corporate structure and market performance.

For that matter, the rich can sink their money into luxuries such as art pieces, sprawling real estate properties, cars, and other collectibles. In this case, they can enjoy grandeur while still benefiting from their increase in value over time. By buying these luxuries, the wealthy not only enhance their lifestyles but also enjoy the value appreciation as a nice bonus.

How the Wealthy Invest

As an example, let’s look at the former CEO of Microsoft, Steve Ballmer. He holds a net worth of about $84 billion in 2021. Even after walking away from Microsoft, Ballmer owns over 300 million shares in the company. This alone translates to a multi-billion-dollar investment.

Some of the other ways Ballmer chose to invest his money included:

A roughly 4% stake in Twitter (before he sold his shares in 2018)

Real estate investments in Hunts Point, Washington, and Whidbey Island

Purchase and ownership of the Los Angeles Clippers basketball team for $2 billion.

The rich can make huge investments in the industries that catch their interest, as shown by the numerous businesspeople who have winded up buying sports teams of one kind or another.

Ballmer’s wealth is concentrated in a handful of investments. This is a far cry from the hundreds of investments that come with Buffett’s and other personal finance gurus’ recommendation of buying low fee index funds.

Hedge funds are likewise popular with the wealthy. These funds of the rich require investors to demonstrate $5,000,000 or more in net worth! The sophisticated strategies intended to beat the market are the allure of the funds. But hedge funds charge approximately 2% of fees and 20% of profits. Investors need to get huge returns to support those high fees!

This isn’t to suggest that the wealthy don’t own traditional stocks, bonds, and fund investments—they do. Yet, their riches and interests open doors to other types of exciting and exclusive investments that aren’t typically available to the average person.

It is true that the wealthy have many opportunities not readily available to the middle and lower class. But this doesn’t necessarily mean they are guaranteed higher rates of return. They won’t always beat index funds, but they more often than not can afford to take on this risk. All in all, they are less dependent on steady growth and returns.

Warren Buffett might be the world’s most famous investor, and he frequently touts the benefits of investing in low-cost index funds. In fact, he’s instructed the trustee of his estate to invest in index funds.

“My advice to the trustee couldn’t be more simple: Put 10% of the cash in short-term government bonds and 90% in a very low-cost S&P 500 index fund.”

-Berkshire Hathaway’s 2013 annual letter to shareholders

If a simple, straightforward low-fee index fund is good enough for Warren Buffett, then it’s certainly adequate for the average investor.

Even though index funds aren’t popular among the very rich, they’re still a great choice for the everyday investor. If that’s the category you identify with, you’d be wise to add some to your portfolio. They may not make you rich overnight. However, by capitalizing on the broad long-term gains of the U.S. market, you could accumulate quite a substantial sum over time and achieve your own financial goals.

Disclosure: Fresh Life Advice is an opinion-based website. I am not a financial advisor, and the opinions on this site should not be considered financial advice.

Personal Capital: The Ultimate Tool to track your Net Worth, Budget and more.

What is your investing strategy? When do you know it’s the right time to buy or sell a stock? Let me know in the comments below.

Disclosure: Fresh Life Advice may receive commissions for affiliate links included in this stocks article. However, we only include links to products that we believe in and utilize ourselves. These recommendations are not given out lightly.

The Main Rules of Fresh Life Advice Stock Investing Strategy

Of all the articles published in this blog’s archives, you can really boil down my incoherent ramblings into a few fundamentals that anyone can use to become a wealthy investor:

Save more than you spend. Live below your means to be able to invest as much money as possible and as early as possible.

Choose passively managed index funds or ETF’s (i.e. NYSEARCA: VTI or MUTF: VTSAX) with the lowest expense ratios (less than 0.15%) in lieu of picking individual stocks, mutual funds with high fees, or actively managed hedge funds.

No short-term active trading. Yes, I’m even talking about the GameStop Stock Frenzy.

Buy and hold for as long as possible, preferably forever. The longer you remain invested, the less “rigged” the market is.

Pick a portfolio allocation and stick to it. Asset allocation trumps stock-picking and a constant search for alpha.

With all that being said, sometimes I will occasionally indulge my animalistic instincts and make speculative plays. In these cases, I am essentially betting on a certain equity (stock) to outperform the market.

But it’s important to realize individual stock investing should not be the majority of your portfolio. We are talking less than 20% of your net worth. Think of it as fun money. If you theoretically lost it all, you would not be devastated.

I know, even losing more than a penny, can be devastating to one’s fragile ego.

INVESTING IN INDIVIDUAL STOCKS

Investing in individual stocks and equities can be overwhelming. There are so many options to choose from. How do you know which will perform well?

The truth is… No one knows.

No one can confidently predict the future without knowing. That’s why investing in low cost index funds is such a trusted solution.

In general, the index funds track the overall market performance. Since indexes like the Standard & Poor’s 500 (S&P 500) are composed of 500 large public stocks, they can capture the stocks that do incredibly well. However, they also contain stocks that possibly underperform or file for bankruptcy.

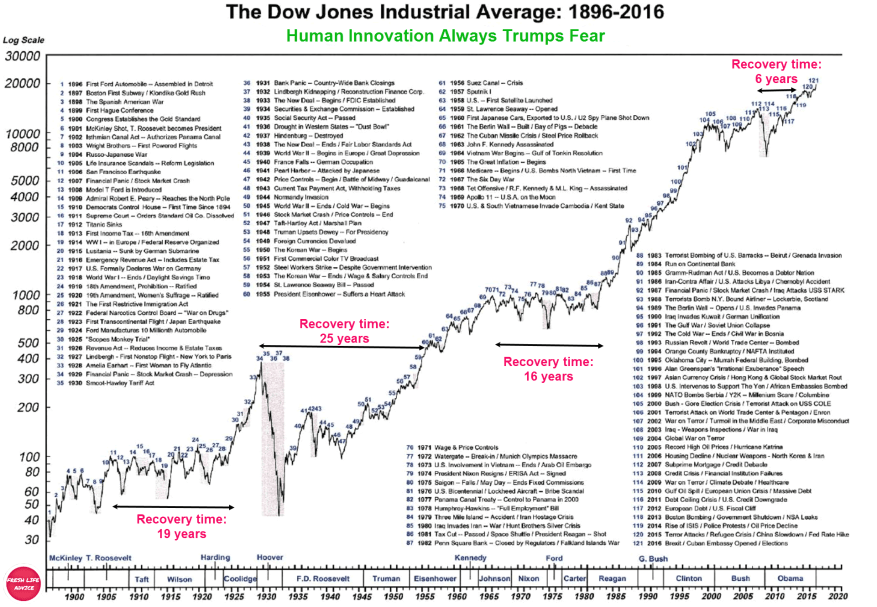

The world usually references the S&P 500 or the Dow Jones Industrial Average as two major indexes that capture the stock market. They are two different indexes, but both are composed of some of the major companies that drive the market.

Although there is no way to tell what the future holds, studying the general market structure and where we are in the current market cycle can help provide a framework for better decision making and future market expectations.

The chart below shows the historical performance of the S&P 500 Index throughout the U.S. Bull and Bear Markets from 1926 all the way up to 2019. It’s imperative to remember past performance is no guarantee of future results. Nevertheless, looking at the history of the market’s expansions and recessions does help to gain a ‘Fresh Life Advice’ perspective on the benefits of investing for the long haul.

On the other hand, the Dow Jones Industrial Average (DJIA) is comprised of 30 large public companies. In the financial industry, the DJIA is used as a benchmark for the largest stock market in the world.

What can you observe from looking at the charts above?

Have a child look at this, and even they will be able to tell you the line goes up over time.

Investing, otherwise known as buying and holding, is notthe same as gambling. If you invest in the market long enough, your investment will increase! Great news for investors!

Due to the former factors, the rate of return for index funds is much more stable than for individual stocks. In other words, the increases and decreases may not be as significant as other equities. This is also what’s known in the finance world as lower volatility.

Stocks are a risky investment vehicle – don’t get me wrong. But index funds are so diversified that it’s nearly impossible for you to lose your entire investment since the fund is unlikely to crash 100% when so many different companies are held in the fund portfolio.

However, as we’ve seen in the past (Covid-19 Correction of March 2020, Financial Crisis of 2008-2009, Dot-Com Bubble of 2000, etc.), investing in individual companies that do go bankrupt can lead to you lose all of your equity in that respective company.

Just remember:

“The markets can stay irrational longer than we can stay solvent…”

– John Maynard Keynes, Economist

Essentially, just because you made the right fundamental investment doesn’t mean the market will treat you fairly. It’s an “Eat-or-be-eaten” world. And the market can easily strip you of all your hard-earned money if you aren’t careful with your risk.

I’m a firm believer that you should never invest in anything that causes you to lose sleep. Dale Carnegie mentions in his famous best-selling book How to Stop Worrying and Start Living.

Without further ado, the two main approaches to use for investing in individual stocks are fundamental analysis and technical analysis.

FUNDAMENTAL ANALYSIS

Fundamental analysis measures stocks by looking at their intrinsic value. For this theory, companies are worth the net present value of their cash flows. Long-term investors study everything from the overall economy and industry conditions to the financial strength and management of individual companies. Earnings, expenses, assets, and liabilities all come under scrutiny by fundamental analysts.

Let’s run through 3 main aspects of fundamentals to check before investing in a stock.

1. Quarterly Earnings

Quarterly earnings are arguably the most important quality of a good stock.

If the company is consistently making money, you will be consistently making money too!

People always like to advise “Let your winners win”. I interpret this as the classic buy and never sell model that Warren Buffett’s mentor, Benjamin Graham, preaches in his book The Intelligent Investor. The underlying basis of this novel is fundamental analysis.

Companies that flaunt consistent earnings beat will see a steady increase in price. This is a major indication that the company is doing something right.

Many investment gurus also claim that past performance does not indicate future results. There is no denying this, but instincts tell us this isn’t painting the whole picture.

Warren Buffett bought more than $1 billion of Coca-Cola (KO) shares in 1988, an amount equivalent to 6.2% of the company, making it the largest position in his portfolio at the time. It remains one of Berkshire Hathaway’s biggest holdings today. Coca-Cola’s iconic name and global reach created a moat around its core soft drink product, so Buffett did not have to worry a competitor would come and take away its market share.

There was a profound perspective Warren touted: no matter who was the CEO of Coca-Cola, the company would still thrive due to the economic powerhouse it had become.

For 99% of the other companies, leadership matters. If a company doesn’t have a strong C-Suite or Board of Directors, the company’s profits may suffer too.

3. PE Ratio

Price-to-Earnings (P/E) Ratio: A ratio used for valuing companies and to find out whether they are overvalued or undervalued.

A highPrice-Earnings ratio indicates that investors are expecting higher growth of company’s earnings in the future compared to companies with a lower Price-Earnings ratio.

A lowPrice-Earnings ratio may indicate either that a company may currently be undervalued or that the company is doing exceptionally well relative to its past trends.

When a company has no earnings or is posting losses, in both cases P/E will be expressed as “N/A.” Though it is possible to calculate a negative P/E, this is not the common convention.